How to get your accounting house in order: a guide for startups

HOME / / How to get your accounting house in order: a guide for startups

* During Coronavirus, we're flagging up key articles about business planning and marketing. We hope this will help you minimise the impact of the current crisis on your business *

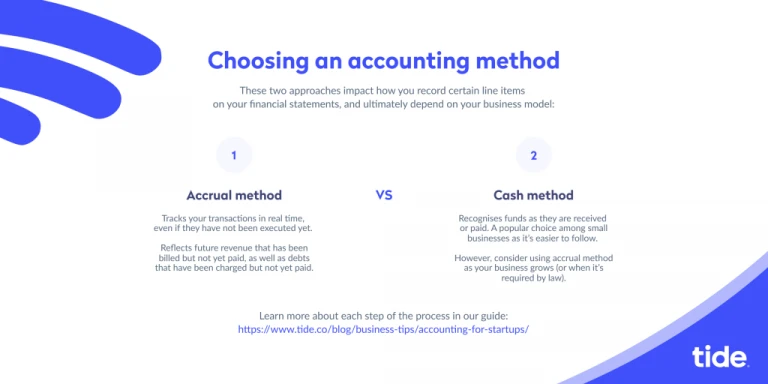

1. Select the right accounting method for your startup

First things first, you need to select an accounting method that’s right for you. There are two primary accounting methods, which are:

Accrual method - recognises when you bill clients or owe money to creditors. This method tracks your transactions in real-time, even if payments are yet to be actioned

Cash method - recognises funds only when they are received or paid. Accounts Receivable or Accounts Payable line items don’t apply.

For most new businesses and startups, we’d recommend the accrual method. Why? Because managing your finances is easier and, depending on your business model/industry, it’s often mandated by law.

Not only that, but accounts receivable and accounts payable will help you keep an eye on transactions, assets and liabilities in real time.

2. Get a solid understanding of these three financial statements

With your accounting method chosen, the next step is to understand the three most common financial statements that you’ll come across when running your startup: your balance sheet, income statements and cash flow statement.

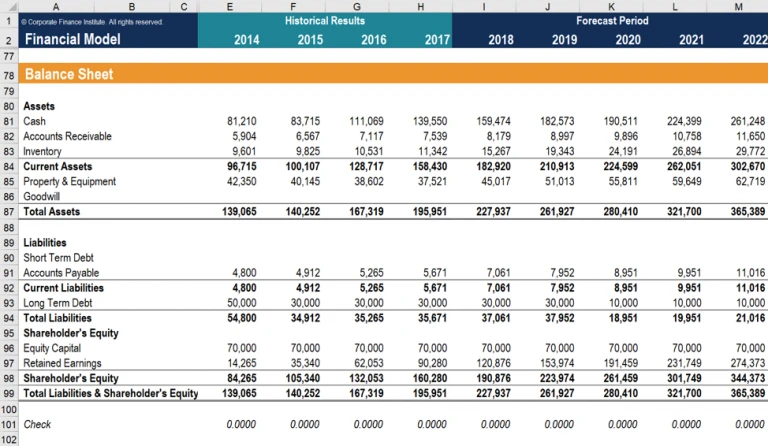

Balance sheet

Your balance sheet illustrates the financial health of your business by showing your assets and liabilities.

Here’s what this looks like (courtesy of CFI).

Your balance sheet includes your:

assets - items your company owns

liabilities - obligations like short-term debts and taxes

equity - what your business is worth

The formula to calculate balance sheet is Assets = Liabilities + Equity.

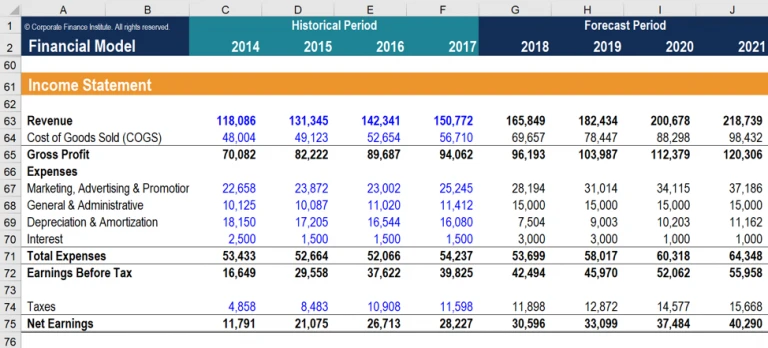

Income statement

Next is your income statement (also known as profit and loss statement).

It provides a financial snapshot that measures how well your startup is performing, and is considered one of the most important financial statements to keep an eye on regularly.

Your income statement can be calculated with the formula Net Income = Revenue – Expenses.

Net income is an important metric, as it illustrates your bottom line after all expenses (including taxes and cost of sales).

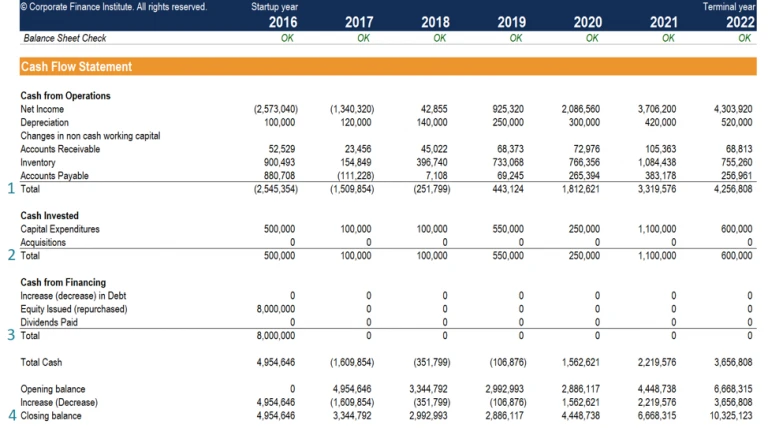

Cash flow statement

Finally, you’ll need your cash flow statement.

This shows you how much cash is flowing in and out of your business across a specific period (eg monthly or quarterly).

Typically, cash flow statements are segmented into three categories:

Operations - activities that contribute to the day-to-day running of your startup

Investing - items and activities that contribute to the growth of your startup

Financing - these are broken down into debt and equity, which highlight activities related to raising investment

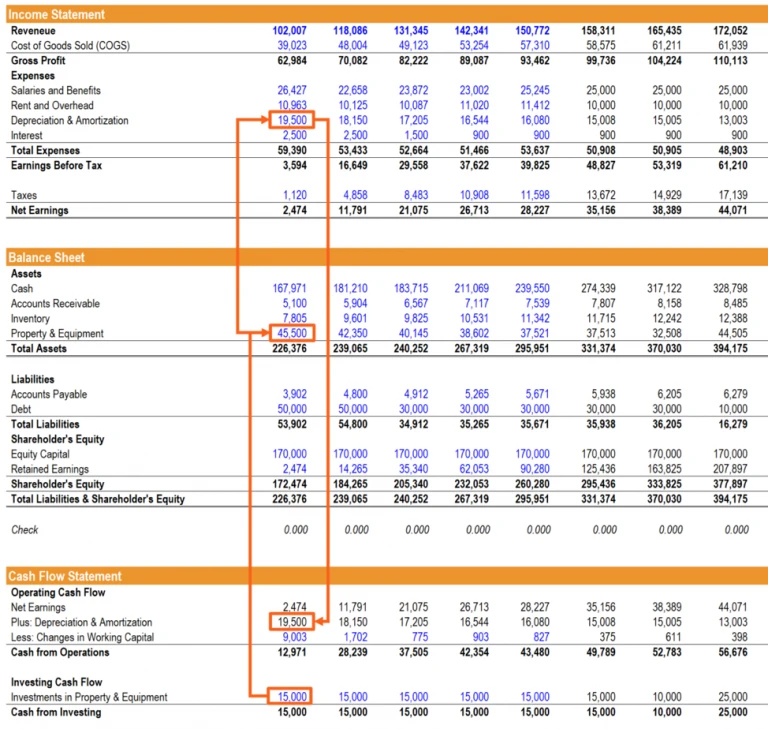

Each of these three statements are related, as demonstrated by this illustration from CFI.

As you can see, the three statements are linked together by specific values:

the net income line on the income statement is linked to both the balance sheet and the cash flow statement

the net income line from the balance sheet then feeds into retained earnings for the owner’s equity

finally, on the cash flow statement, the top line for the cash is linked from the operations section

Knowing how each statement connects, as well as the important line items on each statement, will help you measure the financial health of your startup. In turn, you’re more likely to make decisions that make you profitable, faster.

3. Hiring an accountant, bookkeeper or both?

No matter where your cash is coming from, you still need to ensure it’s contributing to the growth of your startup.

It’s important to have a solid grip on the basics of accounting. But as a startup founder, you’re already focusing on so many things: creating a great product, hiring the best talent and raising funding.

Which is why it’s important to get help, especially in the early days. By recruiting the help of a chartered accountant or bookkeeper, you’ll have an expert set of eyes glancing over your accounts.

The question is, should you hire an accountant, bookkeeper or both?

First, let’s look at the difference between the two:

An accountant has an extensive knowledge in tax law and financial statements. They can help guide you through complex topics and advise you on key financial decisions.

A bookkeeper takes care of basic financial tasks. These include managing income, expenses and bank reconciliation.

Our recommendation? Seek to find someone who can do both.

These days, many agencies and accounting services will take care of both accounting and bookkeeping tasks, and don’t have to cost an arm and a leg.

Getting help early on can save you a host of tax and accounting-related headaches later down the line. At the very least, find someone you can talk to and get advice, no matter where on the fence you sit.

"We’re delighted to be the 2000th loan recipients!"